Phân bổ tài sản đề cập đến cách các nhà đầu tư chia danh mục đầu tư tài trợ của họ giữa các loại tài sản độc quyền dựa trên ước mơ tài chính, khả năng chịu rủi ro và khung thời gian của họ.

Bằng cách đầu tư vào nhiều loại tài sản khác nhau, nhà đầu tư có thể cân bằng rủi ro và lợi nhuận để tối đa hóa lợi nhuận tiềm năng. Phương pháp đa dạng hóa này hình thành nên nguồn cảm hứng cho việc quản lý tài chính thông minh.

Bài viết này sẽ khám phá cách phân bổ tài sản, cách các nhà đầu tư có thể quyết định mức phân bổ tối ưu nhất, cũng như các kỹ thuật triển khai và giám sát việc phân bổ theo thời gian. Chúng tôi sẽ nghiên cứu các vấn đề như điều kiện tài chính có thể ảnh hưởng đến lựa chọn phân bổ như thế nào và những tình huống khó khăn về mặt tinh thần mà các nhà giao dịch thường gặp phải. Mục đích là để giải thích tại sao phân bổ tài sản lại là một ý tưởng quan trọng đối với cả người mới bắt đầu và nhà đầu tư giàu kinh nghiệm để quản lý đúng đắn khoản tiết kiệm khó kiếm được của mình.

Với phương pháp tiếp cận cân bằng, được thiết kế riêng cho từng trường hợp, phân bổ tài sản có thể giúp mọi người đạt được mong muốn tài chính với mức độ rủi ro phù hợp. Bằng cách tiếp tục tìm hiểu, bạn có thể được hưởng lợi từ kiến thức sâu rộng về hoạt động đầu tư quan trọng này và các phương pháp kết hợp nó vào danh mục đầu tư của mình để đạt được thành công lâu dài trên thị trường.

Phân bổ tài sản là gì?

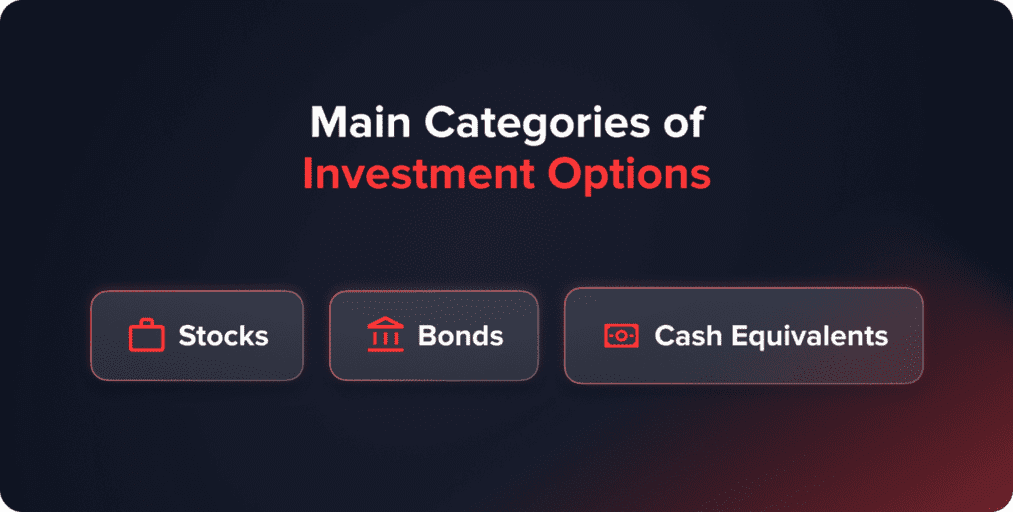

Phân bổ tài sản là quá trình phân chia danh mục đầu tư thành các tài sản tài chính khác nhau, chẳng hạn như cổ phiếu, trái phiếu và các khoản tương đương tiền, với mục tiêu tối ưu hóa rủi ro và lợi nhuận tiềm năng dựa trên khả năng chấp nhận rủi ro và thời hạn đầu tư của nhà đầu tư. Cụ thể hơn, phân bổ tài sản đề cập đến cách nhà đầu tư phân chia danh mục đầu tư của mình thành các loại tài sản chính. Ba loại tài sản chính là cổ phiếu (cổ phiếu), trái phiếu (thu nhập cố định) và tiền mặt/các khoản tương đương tiền.

Bằng cách đầu tư trên khắp các loại tài sản khác nhau , nhà đầu tư có thể hướng đến việc giảm thiểu rủi ro danh mục đầu tư thông qua đa dạng hóa, vì tài sản không phải lúc nào cũng biến động theo cùng một hướng. Ví dụ, khi cổ phiếu giảm, trái phiếu có thể giữ nguyên giá trị hoặc tăng. Cơ cấu phân bổ tài sản phù hợp cho mỗi nhà đầu tư phụ thuộc vào khả năng chịu rủi ro (mức độ biến động mà họ cảm thấy thoải mái) và khung thời gian (khoảng thời gian họ có cho đến khi cần tiếp cận nguồn vốn).

Phân bổ tài sản chiến lược sẽ xem xét các yếu tố này để xác định tỷ lệ đầu tư tối ưu vào cổ phiếu, trái phiếu và tiền mặt nhằm tối đa hóa lợi nhuận cho từng mức độ rủi ro. Phân bổ tài sản là một chiến lược quản lý danh mục đầu tư quan trọng vì nó cho phép nhà đầu tư chấp nhận rủi ro ở mức độ nào đó tùy theo tình hình tài chính và mục tiêu của họ. Việc đa dạng hóa hợp lý thông qua phân bổ tài sản nhằm mục đích cân bằng rủi ro và lợi nhuận tiềm năng.

Tóm lại, phân bổ tài sản là quá trình phân bổ danh mục đầu tư vào các loại tài sản chính để giảm thiểu rủi ro và tối ưu hóa lợi nhuận dựa trên hồ sơ và mục tiêu đầu tư cá nhân. Đây là nguyên tắc cốt lõi để xây dựng danh mục đầu tư toàn diện và cân bằng.

Các loại tài sản chính

Ba loại hình đầu tư chính bao gồm cổ phiếu, trái phiếu và các khoản tương đương tiền. Hãy cùng xem xét kỹ hơn từng loại:

- Cổ phiếu (Equities): Cổ phiếu sở hữu trong các công ty đại chúng mang lại lợi nhuận cao nhất trong dài hạn nhưng cũng thường xuyên có biến động giá trong ngắn hạn.

- Trái phiếu: Essentially loans made to entities and governments, offering interest payments to bondholders but with principal values fluctuating as interest rates change. Trái phiếu tend to be less risky than stocks.

- Tiền mặt tương đương: Tài sản có tính thanh khoản cao như tài khoản tiết kiệm và quỹ thị trường tiền tệ nhằm mục đích bảo toàn vốn của bạn thông qua mức lợi nhuận rất thấp. Được coi là lựa chọn bảo thủ nhất.

Trong các loại tài sản rộng này, tồn tại nhiều phân loại nhỏ cung cấp các hồ sơ rủi ro-lợi nhuận khác nhau. Một số ví dụ bao gồm cổ phiếu vốn hóa lớn so với cổ phiếu vốn hóa nhỏ, thể hiện quy mô công ty, cổ phiếu trong nước so với cổ phiếu quốc tế, và trái phiếu doanh nghiệp xếp hạng đầu tư so với trái phiếu doanh nghiệp rác, với chất lượng tín dụng khác nhau. Ngoài ra còn có trái phiếu chính phủ với các kỳ hạn khác nhau, từ ngắn hạn đến dài hạn, và quỹ tương hỗ chỉ số so với quỹ được quản lý chủ động.

Bạn cũng có thể thích

Vitaly Makarenko

June 26, 2024

Một nguyên tắc cốt lõi trong phân bổ tài sản là lợi nhuận cao đòi hỏi rủi ro cao hơn. Lịch sử đã chứng minh sự đánh đổi giữa rủi ro và lợi nhuận giữa các loại tài sản này, khi cổ phiếu đã vượt trội hơn hẳn các tài sản khác trong nhiều thập kỷ qua nhưng cũng có những đợt suy thoái mạnh theo chu kỳ. Trái phiếu và tiền mặt, mặc dù ít biến động hơn, nhưng lại mang lại lợi nhuận dài hạn khiêm tốn hơn. Bằng cách đa dạng hóa các loại hình đầu tư này, các cá nhân có thể tối ưu hóa danh mục đầu tư của mình để đạt được lợi nhuận tối đa trong phạm vi mức độ chấp nhận rủi ro của họ.

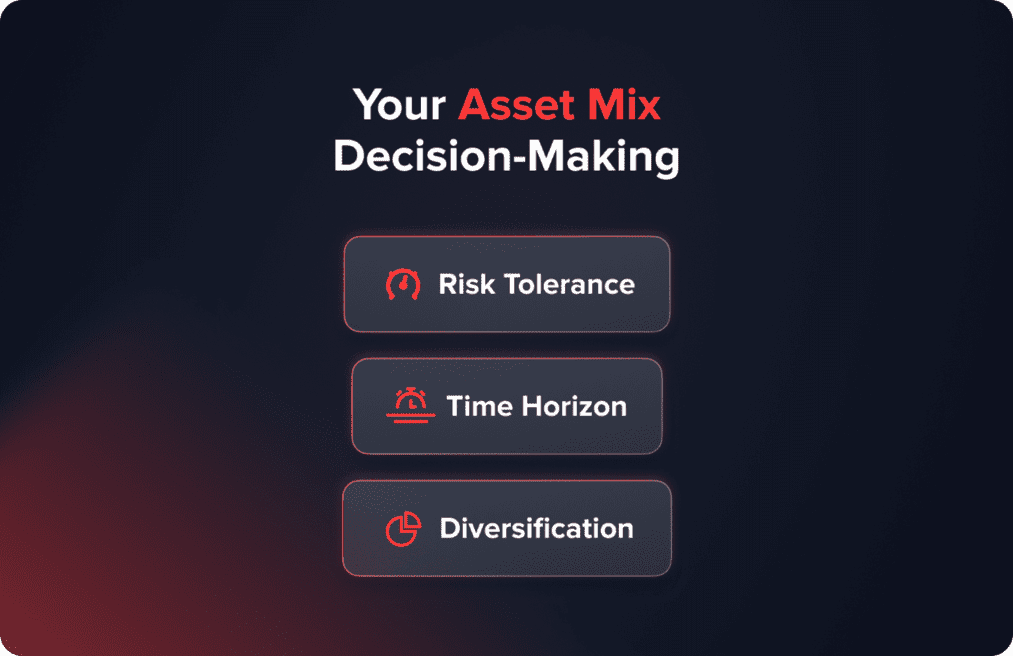

Các khái niệm cốt lõi trong phân bổ tài sản

Ba khái niệm quan trọng giúp hướng dẫn bạn đưa ra quyết định về cơ cấu tài sản:

- Khả năng chịu rủi ro: Bạn có thể thoải mái chịu đựng mức độ biến động về mặt tâm lý đến mức nào

- Đường chân trời thời gian: Khi bạn dự đoán cần phải tiếp cận các quỹ đầu tư

- Đa dạng hóa: Nắm giữ nhiều loại tài sản có mức độ rủi ro bù trừ cho nhau ở nhiều mức độ khác nhau

Bằng cách hiểu các yếu tố này, bạn có thể tối ưu hóa danh mục đầu tư của mình để đạt được lợi nhuận tối đa với mức độ rủi ro có thể chấp nhận được dựa trên mục tiêu cá nhân, mốc thời gian và khả năng chịu đựng những biến động ngắn hạn của thị trường.

Xác định phân bổ tài sản của bạn

Việc xây dựng danh mục tài sản tối ưu đòi hỏi phải phân tích nhiều yếu tố cá nhân cụ thể. Bằng cách xem xét kỹ lưỡng từng yếu tố ảnh hưởng, nhà đầu tư có thể thiết kế một danh mục đầu tư phù hợp với mục tiêu và tính cách của mình. Một số khía cạnh quan trọng định hình mức độ chấp nhận rủi ro và tỷ trọng tài sản phù hợp:

- Tuổi: Các nhà đầu tư trẻ tuổi có hàng thập kỷ trước khi bước vào những sự kiện quan trọng trong đời, cho phép họ linh hoạt chấp nhận rủi ro trong những năm đầu sự nghiệp để tìm kiếm sự tăng trưởng. Những người sắp nghỉ hưu ưu tiên bảo toàn vốn khi thời gian để bù lỗ ngày càng ngắn lại.

- Mục tiêu tài chính: Những mục tiêu như tiết kiệm để mua nhà trong vòng 5 năm đòi hỏi cách phân bổ khác với việc tích lũy tiền tiết kiệm trong 40 năm để có cuộc sống thoải mái sau khi nghỉ hưu. Mục tiêu càng xa, việc phân bổ càng cần phải quyết liệt hơn khi muốn tối đa hóa lợi nhuận trong một thời gian dài.

- Khả năng chịu rủi ro: Khả năng chịu đựng biến động ngắn hạn trong khi vẫn duy trì được tầm nhìn dài hạn của mỗi cá nhân khác nhau tùy thuộc vào tính cách, tài sản hiện có và khả năng phục hồi sau những đợt suy thoái tiềm ẩn. Mức độ chịu đựng sẽ quyết định mức độ tiếp cận vốn chủ sở hữu phù hợp.

Hướng dẫn phân bổ chung

Một quy tắc thường được trích dẫn sử dụng độ tuổi để ước tính mức độ tiếp xúc với cổ phiếu. Phương pháp này đề xuất lấy 110 trừ đi tuổi của bạn để xác định tỷ lệ phân bổ cổ phiếu. Ví dụ, ở độ tuổi 40, công thức sẽ cho thấy danh mục đầu tư của bạn nên có 70% cổ phiếu (110 – 40 = 70). Tuy nhiên, các mô hình đơn giản này hiếm khi giải quyết được những vấn đề cá nhân phức tạp.

Các điểm tham chiếu mang tính hướng dẫn hơn là các danh mục đầu tư mô hình giả định thể hiện các chiến lược thận trọng, cân bằng và tích cực. Các danh mục đầu tư thận trọng (20-40% cổ phiếu) nhấn mạnh quản lý rủi ro hơn lợi nhuận. Các danh mục đầu tư vừa phải (40-60% cổ phiếu) cân bằng hai ưu tiên này. Các danh mục đầu tư tích cực (60-80% cổ phiếu) tập trung vào tăng trưởng dài hạn thông qua việc tối đa hóa mức độ tiếp xúc với cổ phiếu.

Việc so sánh khả năng chịu đựng và thời gian của một người với các danh mục đầu tư mẫu khác nhau là một điểm khởi đầu hữu ích. Tuy nhiên, việc cá nhân hóa là chìa khóa, vì không có hai tình huống tài chính nào giống hệt nhau. Sức khỏe khác nhau, người phụ thuộc, sự biến động thu nhập, rủi ro nghề nghiệp, v.v. đòi hỏi sự cân nhắc tùy chỉnh.

Các cố vấn giàu kinh nghiệm có thể xây dựng các phân bổ riêng biệt, tính đến nhu cầu đa dạng và mức độ thoải mái. Thay vì chỉ dựa vào công thức, việc xem xét các giai đoạn sự nghiệp riêng biệt, người phụ thuộc, sự ổn định công việc, và khả năng thu nhập hoặc thừa kế trong tương lai sẽ giúp phân bổ phù hợp cho từng giai đoạn. Kế hoạch cá nhân hóa đảm bảo khả năng chấp nhận rủi ro phù hợp để đạt được mục tiêu bất chấp những điều kiện thay đổi.

Thực hiện và duy trì phân bổ tài sản của bạn

Sau khi xác định được cơ cấu tài sản phù hợp, bước quan trọng tiếp theo là lựa chọn các công cụ để thực hiện kế hoạch một cách hiệu quả theo thời gian. Có một số lựa chọn chi phí thấp:

- Các quỹ chỉ số thị trường rộng cung cấp danh mục đầu tư đa dạng với chi phí tối thiểu bằng cách theo dõi thụ động các phân khúc như cổ phiếu và trái phiếu trong nước/quốc tế. Điều này cho phép bao quát mọi cơ sở với chi phí phải chăng.

- ETF (quỹ giao dịch trên sàn chứng khoán) cung cấp khả năng tương tự trong việc xây dựng danh mục đầu tư đa dạng hóa toàn cầu, tiết kiệm chi phí, nhắm vào các yếu tố cụ thể thông qua nhiều phương tiện đầu tư chính xác.

- Quỹ mục tiêu ngày tự động tái cân bằng danh mục đầu tư đã được điều chỉnh rủi ro và thiết lập trước, ngày càng thận trọng hơn khi năm nghỉ hưu mục tiêu đến gần. Điều này mang lại khả năng quản lý đơn giản, không cần can thiệp, phù hợp với lịch trình của mỗi người.

- Các cố vấn robot xây dựng danh mục đầu tư được quản lý kỹ thuật số tùy chỉnh dựa trên hồ sơ rủi ro và mục tiêu của nhà đầu tư, duy trì giám sát liên tục với mức phí thấp so với các cố vấn truyền thống.

Bất kể việc triển khai phương tiện như thế nào, việc bảo trì định kỳ vẫn rất quan trọng. Biến động tự nhiên của thị trường chắc chắn sẽ làm thay đổi tỷ lệ phần trăm theo năm, đòi hỏi phải có các giao dịch tái cân bằng định kỳ để khôi phục mức phân bổ rủi ro dự kiến. Sự trôi dạt không được kiểm soát có thể làm suy yếu các mục tiêu chiến lược.

Bạn cũng có thể thích

Vitaly Makarenko

May 1, 2024

Ngoài ra, những thay đổi về vật chất trong cuộc sống đòi hỏi phải liên tục xem xét và điều chỉnh. Các sự kiện kích hoạt phân tích mới có thể bao gồm hôn nhân, con cái, mất việc, thừa kế hoặc các ưu tiên đang thay đổi. Việc đảm bảo danh mục đầu tư phát triển cùng với những nhu cầu thay đổi sẽ tối ưu hóa cơ hội đạt được các mục tiêu cá nhân năng động. Việc giám sát thường xuyên duy trì logic chiến lược năng động khi các tình huống thay đổi trong cuộc sống.

Việc thực hiện có hệ thống và duy trì có trách nhiệm kết hợp sẽ tạo nên nền tảng cần thiết để thực hiện vai trò cơ bản của việc phân bổ tài sản như một khuôn khổ xây dựng sự giàu có lâu dài phù hợp với từng bản sắc tài chính riêng biệt.

Tác động của kinh tế và thị trường đến phân bổ tài sản

Có lẽ những yếu tố ảnh hưởng lớn nhất đến việc phân bổ tài sản chiến lược là tình hình kinh tế hiện tại và hiệu suất của thị trường tài chính. Các nhà đầu tư thận trọng phải cân nhắc kỹ lưỡng trước những thay đổi này theo thời gian. Trong giai đoạn kinh tế tăng trưởng và thị trường chứng khoán tăng trưởng, cổ phiếu thường vượt trội hơn các tài sản khác khi lợi nhuận doanh nghiệp tăng đều đặn. Do đó, danh mục đầu tư hướng đến tăng trưởng thường tập trung vào cổ phiếu phù hợp với điều kiện mở rộng.

Tuy nhiên, suy thoái kinh tế và suy thoái thường đi kèm với giá cổ phiếu giảm trong ngắn hạn khi bất ổn gia tăng. Vào những thời điểm như vậy, một lập trường thận trọng hơn, tập trung vào thu nhập cố định và tiền mặt, sẽ bảo toàn vốn tốt hơn bằng cách tránh suy thoái. Môi trường lãi suất cũng đòi hỏi một phản ứng nhanh nhạy. Lãi suất tăng khiến giá trái phiếu giảm, tạo điều kiện cho các khoản nợ ngắn hạn hoặc cổ phiếu. Ngược lại, các đợt lạm phát tăng lên làm tăng sức hấp dẫn của trái phiếu, hàng hóa và bất động sản gắn liền với lạm phát, mang lại sự bảo vệ khỏi lạm phát.

Thay vì thiết lập danh mục đầu tư theo kiểu "đặt rồi quên", việc thường xuyên đánh giá các tín hiệu kinh tế vĩ mô và thị trường vốn sẽ giúp xác định thời điểm chuyển đổi phân bổ giữa các vị thế tấn công, phòng thủ hoặc tập trung vào chất lượng. Việc tái cấu trúc danh mục theo các điều kiện hiện tại sẽ tối ưu hóa lợi nhuận điều chỉnh theo rủi ro qua các chu kỳ khác nhau. Việc theo dõi chặt chẽ các yếu tố cầu mạnh mẽ này giúp ngăn ngừa các chiến lược cũ kỹ, trì trệ bỏ qua các yếu tố cơ bản luôn thay đổi. Một phương pháp tiếp cận năng động, phản ứng một cách có hệ thống với các thay đổi vẫn là một giải pháp thận trọng khi tình hình thay đổi theo biến động của thị trường kinh doanh và tín dụng.

Những sai lầm và thách thức thường gặp

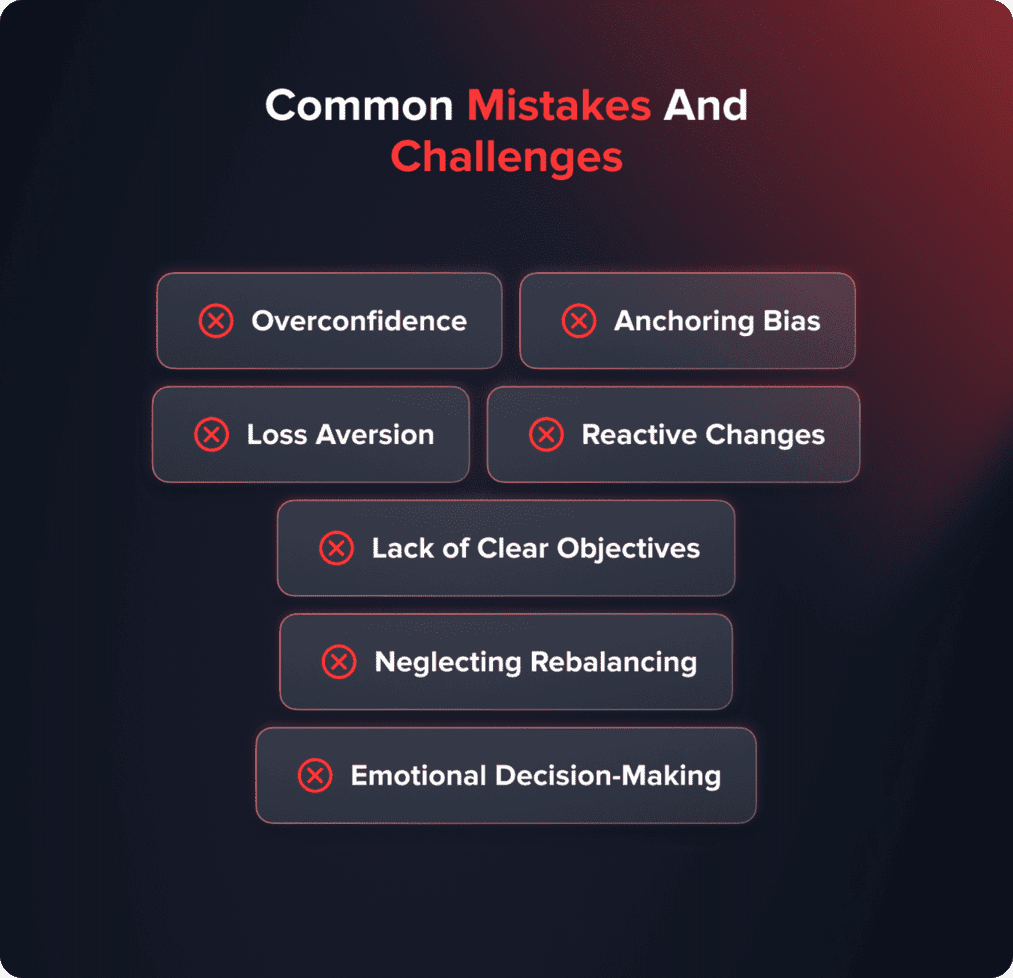

Mặc dù việc phân bổ tài sản cung cấp một khuôn khổ hợp lý, nhưng những khuynh hướng tâm lý bẩm sinh có thể phá hoại ngay cả những kế hoạch được xây dựng kỹ lưỡng nhất nếu không được nhận ra. Việc tự nhận thức được những thành kiến này là chìa khóa cho thành công lâu dài.

- Sự tự tin thái quá dẫn đến thiên kiến gần đây, cho rằng các điều kiện gần đây sẽ tiếp diễn thay vì quay trở lại các chuẩn mực dài hạn. Điều này khiến nhiều người chạy theo đà tăng trưởng của thị trường khi thị trường đạt đỉnh.

- Sự thiên vị neo giữ làm sai lệch các quyết định dựa trên kết quả ban đầu thay vì xem xét tất cả thông tin có sẵn một cách khách quan.

- Tâm lý sợ mất mát tạo ra sự tê liệt trong thời kỳ suy thoái, đúng vào lúc việc tái đầu tư sẽ mang lại lợi ích cao nhất. Cũng như cảm xúc dâng trào trong thời điểm khó khăn, thiên kiến nhận thức cũng nổi lên mạnh mẽ nhất.

- Những thay đổi phản ứng tập trung vào tiếng ồn ngắn hạn hơn là hoàn cảnh cá nhân làm thất vọng sự thật quản lý rủi ro . Chỉ có những điều chỉnh sau khi sửa chữa mới là quá muộn.

- Việc xác định rõ ràng mục tiêu và mức độ chấp nhận rủi ro ngay từ đầu sẽ giúp tăng khả năng chịu trách nhiệm trong bối cảnh biến động không thể tránh khỏi.

- Việc tự động cân bằng định kỳ sẽ loại bỏ sự phấn khích hoặc lo lắng sắp xảy ra, tuân theo quan điểm dài hạn.

- Việc đánh giá có lương tâm sẽ chống lại xu hướng đưa ra quyết định thiếu thận trọng khi cảm xúc biến động lên đến đỉnh điểm.

Bằng cách hiểu rõ những lỗi kinh nghiệm điển hình, nhà đầu tư có thể tránh được tình trạng hao hụt tài sản thông qua việc cam kết duy trì phân bổ tài sản một cách có kỷ luật, phù hợp với chiến lược đã định thay vì cảm tính nhất thời. Sự tự nhận thức mở đường cho thành công lâu dài.

Kết luận

Phân bổ tài sản cung cấp một phương pháp tiếp cận đầu tư nền tảng bằng cách đa dạng hóa các danh mục rủi ro và lợi nhuận bổ sung, phù hợp với mục tiêu cá nhân, khả năng chấp nhận rủi ro và thời hạn đầu tư. Khi được thiết kế chu đáo, cân nhắc kỹ lưỡng nhiều yếu tố cá nhân và linh hoạt thích ứng với nhu cầu và môi trường thay đổi theo thời gian, đa dạng hóa chiến lược cho phép tối đa hóa lợi nhuận trên mỗi đơn vị rủi ro được chấp nhận.

Tuy nhiên, việc bảo trì liên tục bao gồm việc xem xét định kỳ và tái cân bằng là rất quan trọng, cũng như quan điểm khách quan, dựa trên cơ sở lý luận, để khắc phục những thành kiến về hành vi có thể làm suy yếu khả năng của khuôn khổ trong việc thực hiện hiệu quả vai trò quan trọng của nó trong việc tích lũy của cải lâu dài phù hợp với từng tình huống cụ thể.