Navigating the complexities of the financial market demands more than just a keen eye for trends and an understanding of economic indicators; it requires a robust framework for managing risks. Effective broker risk management is the backbone of any successful brokerage, ensuring that potential threats are identified, assessed, and mitigated promptly. This process not only safeguards the brokerage’s assets but also instills confidence in clients, which is paramount for sustaining long-term relationships and stability in the market. By understanding and implementing best practices in broker risk management, brokers can navigate the volatile waters of the financial markets with greater assurance and success.

Risk Identification and Assessment

The cornerstone of effective broker risk management is the meticulous identification and assessment of risks. This foundational step involves a thorough and systematic analysis of all potential risks that could adversely affect the brokerage’s operations. By categorizing these risks into market, credit, and operational risks, brokers can develop targeted strategies to manage each type effectively.

Market Risks

Market risks, the most apparent and often the most volatile, stem from fluctuations in asset prices, changes in market volatility, interest rates, and broader economic trends. These risks are inherent to trading and investing activities. Fluctuations in asset prices can result from various factors, including economic data releases, geopolitical events, and changes in investor sentiment. Interest rate changes can affect the cost of borrowing and the returns on investments, impacting both equity and bond markets. Broader economic trends, such as recessions or periods of high inflation, can also lead to significant market volatility. Identifying market risks involves using analytical tools and financial models to predict potential market movements and quantify potential losses.

You may also like

Vitaly Makarenko

May 1, 2024

Credit Risks

Credit risks arise from the possibility that counterparties may default on their obligations, leading to financial losses for the brokerage. These risks are particularly pertinent in transactions involving credit, such as loans, bonds, and other forms of debt. Evaluating credit risks requires a comprehensive assessment of a counterparty’s financial health, including their credit history, repayment capacity, and overall financial stability. This evaluation often involves analyzing financial statements, credit ratings, and market reputation. Continuous monitoring of counterparties is essential to detect any signs of deteriorating credit quality early.

Operational Risks

Operational risks involve the potential for losses resulting from inadequate or failed internal processes, systems, human errors, or external events. These risks can manifest in various ways, including system failures, fraud, data breaches, and process inefficiencies. Identifying operational risks requires a detailed examination of internal operations, including IT infrastructure, process workflows, and employee actions. Regular audits and reviews of internal controls help identify vulnerabilities that could lead to operational disruptions. Human errors, such as data entry mistakes or unauthorized actions, also fall under this category and require robust training and monitoring programs to mitigate.

Legal Risks

Legal risks arise from potential legal actions, regulatory changes, or breaches of compliance that can impact the brokerage’s operations and financial stability. These risks can result from failing to adhere to laws and regulations, such as securities regulations, data protection laws, and anti-money laundering requirements. Legal risks also include potential lawsuits or enforcement actions taken by regulatory bodies. Identifying legal risks involves staying informed about current and upcoming regulations, ensuring that contracts and agreements are legally sound and enforceable, and maintaining a dedicated compliance team to monitor and implement necessary regulatory changes.

Reputational Risks

Reputational risks involve potential damage to the brokerage’s reputation resulting from negative publicity, regulatory breaches, or poor client experiences. These risks can lead to a loss of client trust and a decline in business. Factors contributing to reputational risks include public scandals, customer complaints, regulatory fines, and negative media coverage. Identifying reputational risks requires ongoing monitoring of public perception through tools such as social media tracking, client surveys, and reputation management software. Feedback from clients and stakeholders can provide early warnings of issues that may harm the brokerage’s reputation.

By meticulously identifying and assessing these risks, brokers can develop targeted strategies to mitigate them, thereby safeguarding their operations and ensuring long-term stability and success in the financial markets.

Other Risks

AI and Algorithmic Risk: The “Rogue Code” Problem

By 2026, the “trader” on the other side of the screen is more likely to be a line of code than a human being. While algorithmic trading brings volume and efficiency, it introduces Algorithmic Contagion. A poorly coded AI can enter thousands of erroneous trades in seconds, potentially draining a broker’s capital or crashing their server before a human risk manager even notices the alert.

The solution is a hard-coded Kill Switch. This is an automated “emergency brake” that sits outside the trading platform. If an account’s activity hits a pre-set threshold—such as an unnatural spike in order frequency or a sudden 15% drop in equity—the Kill Switch instantly severs the connection and flattens the positions. Beyond the emergency brake, brokers must also watch for Model Drift, where an AI that worked perfectly in a trending market begins to fail (and “revenge trade”) when the market turns sideways.

Behavioral Risk: Identifying the “Toxic” Trader

Not all profitable traders are a threat, and not all losing traders are “safe” for a broker. Smart risk management involves looking at Behavioral Flow. Some traders use “toxic” strategies, like Latency Arbitrage, where they use high-speed connections to exploit tiny price delays between different brokers. They aren’t predicting the market; they are “gaming” the broker’s technical infrastructure.

By profiling client behavior, risk managers can distinguish between Healthy Flow (traders using genuine analysis) and Toxic Flow (those exploiting system weaknesses). The strategy here is simple: keep the healthy, predictable flow on your B-Book to internalize the spread, but immediately move “toxic” or high-frequency predatory traders to the A-Book. This passes the risk directly to the larger liquidity providers and protects your firm from being “picked off” by specialized bots.

Healthy Flow vs. Toxic Flow

| Feature | Healthy Retail Flow | Toxic / Predatory Flow |

| Trade Duration | Minutes to Days | Milliseconds to Seconds |

| Strategy | Technical/Fundamental Analysis | Latency Arbitrage or News Hacking |

| Execution | Market orders during normal hours | Heavy volume during “thin” liquidity |

| Broker Action | Keep on B-Book (Internalize) | Move to A-Book (Pass to LP) |

Beyond Gut Feeling: The Math of Risk

While experience is great, you can’t manage what you can’t measure. Brokers use specific mathematical “guardrails” to make sure a bad day doesn’t turn into a terminal one. These aren’t just abstract formulas; they are the benchmarks for how much “skin in the game” a broker can afford.

- Value at Risk (VaR): Think of this as your “sleep at night” number. It tells you, with $99\%$ certainty, what your maximum loss could be over the next 24 hours.

- Expected Shortfall (CVaR): If VaR is the “storm warning,” Expected Shortfall is the “flood insurance.” It looks at the absolute worst-case scenarios—the ones that happen in the $1\%$ of cases where VaR is exceeded. It asks: “If everything goes wrong, how bad does it actually get?”

- Stress Beta: Markets behave differently when they’re panicking. Stress Beta measures how your portfolio’s “personality” changes during a crisis, ensuring you aren’t caught off guard when assets that usually move in different directions suddenly start crashing together.

Survival of the Fittest: Margin & Leverage

Leverage is a powerful tool, but it’s also the fastest way to go out of business if handled poorly. The real challenge for a broker is managing Margin Risk—ensuring that a client’s excitement doesn’t become the firm’s liability.

The industry is moving away from “set it and forget it” margin rules. Instead, many now use Dynamic Margin. If a massive economic announcement is coming up or a specific currency is looking shaky, the system automatically dials back the available leverage. This prevents the dreaded “Negative Balance” disaster, where a client’s account drops below zero so fast that the broker is left holding the bill for their losses. It’s about being the “adult in the room” when the market gets rowdy.

The Human Element: Building a Risk Culture

You can have the best software in the world, but it won’t save you if your team is cutting corners. A true Risk Culture means that staying safe is everyone’s job, not just the “Compliance Officer’s” problem.

This starts with the people at the top. If leadership rewards reckless growth over steady stability, the staff will follow suit. It’s about aligning incentives—making sure bonuses aren’t just tied to how much money a desk brings in, but how safely they brought it in. It also means keeping everyone’s eyes peeled for “bad actors” using tactics like spoofing or layering. At the end of the day, a broker’s strongest shield is a team that understands that protecting the firm’s reputation is just as important as protecting its capital.

Risk Mitigation Strategies

Once risks are identified and assessed, implementing effective risk mitigation strategies becomes paramount. These strategies are designed to reduce both the likelihood and impact of identified risks, ensuring the brokerage’s stability and resilience. Here are some of the most effective risk mitigation strategies.

Diversification

Diversification is a cornerstone of risk mitigation in the brokerage industry. By spreading investments across various asset classes, sectors, and geographical regions, brokers can significantly reduce the impact of adverse movements in any single market or asset.

- Asset Class Diversification: Investing in a mix of stocks, bonds, commodities, real estate, and other asset classes can help balance risk. For instance, when stock markets are volatile, bonds might offer stability. Diversification within asset classes, such as holding various types of bonds (government, corporate, municipal), can also provide added protection.

- Sector Diversification: Within asset classes, spreading investments across different sectors (e.g., technology, healthcare, finance) can protect against sector-specific downturns. If the technology sector experiences a downturn, investments in healthcare or finance might still perform well. Sector rotation strategies, which involve shifting investments between sectors based on economic cycles, can enhance diversification benefits.

- Geographical Diversification: Investing in different geographical regions can mitigate risks associated with country-specific economic or political events. For example, while one country might face economic challenges, another might thrive. Emerging markets can offer growth opportunities, while developed markets might provide stability.

- Investment Vehicles: Utilizing various investment vehicles such as mutual funds, ETFs, and index funds can offer diversification within a single product, providing exposure to a broad range of assets with relatively low cost and management effort. These vehicles can provide access to niche markets or specific strategies (e.g., sector-specific ETFs, thematic mutual funds) that might be difficult to achieve through direct investment.

- Time Diversification: Spreading investments over different time horizons can reduce market timing risk. By dollar-cost averaging, where investments are made at regular intervals, brokers can mitigate the impact of market volatility on the overall portfolio.

Hedging

Hedging involves using financial instruments to offset potential losses from adverse price movements. Effective hedging requires a deep understanding of financial markets and instruments.

- Options: Options provide the right, but not the obligation, to buy or sell an asset at a predetermined price. For example, purchasing put options can protect against significant declines in stock prices, as they give the right to sell the stock at a specific price, thus capping potential losses. Call options can be used to lock in purchase prices for assets that are expected to rise.

- Futures and Forwards: These contracts obligate the buyer to purchase, or the seller to sell, an asset at a predetermined future date and price. For instance, brokers can hedge against currency risk by entering into forward contracts that lock in exchange rates, protecting against unfavorable currency fluctuations. Futures can be used to hedge commodities, interest rates, or stock indices.

- Swaps: Swaps involve exchanging cash flows or other financial instruments between parties. Interest rate swaps can hedge against changes in interest rates. In contrast, credit default swaps (CDS) can protect against credit risk by transferring the risk of a counterparty default to another party. Currency swaps can manage exchange rate risks in international investments.

- Hedging Costs and Benefits: Balancing the costs of hedging with the potential benefits is crucial. While hedging can reduce risk, it also involves costs such as premiums for options or margin requirements for futures. Brokers must carefully assess whether the cost of hedging justifies the protection it offers. Understanding the Greeks (Delta, Gamma, Theta, Vega, Rho) in options trading can help evaluate the cost-effectiveness of hedging strategies.

- Dynamic Hedging: Adjusting hedging strategies in response to changing market conditions can optimize protection. This involves regularly reviewing and rebalancing hedging positions to ensure they remain effective.

You may also like

Demetris Makrides

July 26, 2024

Risk Limits and Monitoring

Establishing risk limits is essential for controlling exposure to various risks. These limits should be aligned with the brokerage’s risk appetite and financial capacity. Continuous monitoring ensures that exposures remain within acceptable levels.

- Setting Risk Limits: Risk limits can be set based on various criteria, including asset class, sector, geographical region, and individual counterparty exposure. These limits should reflect the brokerage’s overall risk tolerance and strategic objectives. For example, setting a maximum percentage of the portfolio that can be invested in high-risk assets ensures balanced risk exposure.

- Real-Time Monitoring: Automated risk management systems can provide real-time data and alerts, enabling brokers to take timely actions to mitigate risks. These systems can track market movements, counterparty exposures, and compliance with risk limits, offering a comprehensive view of the brokerage’s risk profile. Artificial intelligence and machine learning integration can enhance predictive analytics and risk assessment capabilities.

- Stress Testing and Scenario Analysis: Regular stress testing and scenario analysis help ensure adequate risk limits under extreme market conditions. These tests can reveal potential vulnerabilities and guide adjustments to risk limits and hedging strategies. Scenario analysis can include hypothetical events such as market crashes, economic recessions, or geopolitical tensions.

- Dynamic Adjustments: Risk limits and monitoring processes should be dynamic, allowing for adjustments in response to changing market conditions, regulatory requirements, and the brokerage’s evolving risk profile. Risk management practices must be continuously reviewed and adapted to maintain effective control. Implementing a risk dashboard that provides a real-time overview of key risk indicators can facilitate prompt decision-making.

Contingency Planning

In addition to diversification, hedging, and monitoring, brokers should develop robust contingency plans to address potential risk events.

- Crisis Management Plans: Detailed crisis management plans to ensure brokers can respond quickly and effectively to unexpected events. These plans should outline procedures for communication, decision-making, and operational adjustments during a crisis. Regular training and drills can ensure that all staff are familiar with the crisis management protocols.

- Liquidity Reserves: Maintaining adequate liquidity reserves is essential for managing financial stress. Liquidity reserves can provide the necessary buffer to cover unexpected losses or meet margin calls without disrupting normal operations. Strategies to enhance liquidity include maintaining a portion of the portfolio in highly liquid assets and establishing lines of credit with financial institutions.

- Business Continuity Planning: Business continuity plans ensure that critical functions can continue during and after a disruption. This includes IT disaster recovery plans, alternative trading platforms, and backup data centers. Regular testing and updating of business continuity plans ensure they remain effective and relevant.

- Communication Strategies: Effective crisis communication with clients, employees, and regulators is crucial. Transparent and timely communication can help manage expectations and maintain trust. Establishing a communication protocol and designating spokespeople can streamline this process.

By implementing these comprehensive risk mitigation strategies, brokers can significantly reduce their exposure to various risks, ensuring the stability and resilience of their operations. Effective risk management protects the brokerage’s assets and builds trust and confidence among clients, fostering long-term success in the financial markets.

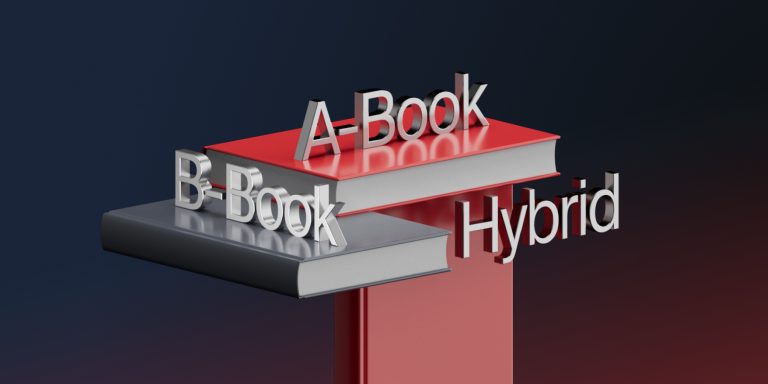

Comparing Brokerage Execution Models

Choosing a business model is the most significant risk management decision a broker makes. It dictates whether you are taking on market risk yourself or passing it to others.

| Feature | A-Book (STP/ECN) | B-Book (Market Maker) | Hybrid Model |

| How it Works | Trades are passed directly to liquidity providers. | The broker takes the opposite side of the client’s trade. | Small/risky trades are B-booked; large/pro trades are A-booked. |

| Source of Profit | Commissions and spread markups. | Client losses and wider spreads. | Mix of commissions and trading P&L. |

| Market Risk | Low. The broker is market-neutral. | High. If clients win, the broker loses. | Managed. Uses client profiling to offset risk. |

| Conflict of Interest | None. The broker wants the client to trade more. | High. The broker profits when the client loses. | Low to Moderate. |

| Best For | Professional & high-volume traders. | Small retail accounts and beginners. | Growing brokerages wanting the “best of both worlds.” |

You may also like

Demetris Makrides

January 17, 2024

The Digital Fortress: Technology & Cyber Resilience

In today’s world, a broker’s biggest threat isn’t just a market crash—it’s a keyboard. Cybersecurity has shifted from a back-office IT task to the very front line of risk management. We’ve moved past the days when a simple firewall was enough; today’s standard is Zero Trust. Essentially, the system assumes every entry point is a potential threat until proven otherwise.

It’s not just about stopping hackers from stealing data; it’s about protecting the “heartbeat” of the firm: the Order Management System (OMS). A single minute of downtime or a “flash crash” caused by a software glitch can burn through years of built-up trust. Forward-thinking brokers are now using AI not just to trade, but to hunt for “digital smoke”—small, unusual patterns in data or logins that suggest a breach is brewing before the fire actually starts.

Regulatory Compliance

Adhering to regulatory requirements is a critical aspect of broker risk management. Regulations are designed to ensure market integrity, protect investors, and promote financial stability. Brokers must stay informed about relevant regulations and ensure compliance to avoid legal penalties and reputational damage.

Maintaining Accurate Records

Brokers must maintain accurate and comprehensive records of all transactions, client interactions, and financial activities. These records are crucial for audits, regulatory reviews, and ensuring transparency. Implementing robust record-keeping systems that are regularly updated can help brokers meet these requirements efficiently. Digitization of records and using secure cloud storage solutions can enhance accessibility and security.

Performing Due Diligence

Due diligence involves thoroughly investigating and verifying clients’ backgrounds, financial status, and investment objectives. This process is essential for preventing fraud, money laundering, and other illicit activities. Brokers should utilize advanced due diligence tools and databases to verify client information. Enhanced due diligence procedures involving deeper investigation and continuous monitoring may be necessary for high-risk clients or transactions.

Anti-Money Laundering and Know Your Customer Procedures

Implementing AML and KYC procedures is mandatory to prevent illicit activities. AML programs should include risk assessment, client identification, transaction monitoring, and reporting suspicious activities to relevant authorities. KYC involves verifying clients’ identities, understanding their financial activities, and assessing potential risks. Regular updates to client information and ongoing monitoring are crucial for effective AML and KYC compliance. Training staff on AML and KYC requirements ensures that procedures are consistently followed.

Compliance Checks and Audits

Regular internal and external audits are essential for identifying and rectifying non-compliance issues. Internal audits should be conducted periodically to review compliance with regulatory requirements, internal policies, and risk management practices. External audits by independent auditors can objectively assess the brokerage’s compliance status. Implementing audit recommendations promptly and effectively can enhance compliance and mitigate risks.

Conclusion

In conclusion, effective broker risk management involves a systematic approach to identifying, assessing, and mitigating risks. By adopting best practices and continuously improving their risk management strategies, brokers can safeguard their operations, protect their clients, and achieve sustainable success in the financial markets.