ความโค้งเป็นการวัดความสัมพันธ์ระหว่างราคาพันธบัตรและอัตราดอกเบี้ย มันอธิบายว่าทำไมราคาพันธบัตรจึงไม่เคลื่อนที่ในเส้นตรงอย่างสมบูรณ์เมื่ออัตราดอกเบี้ยเปลี่ยนแปลง ในขณะที่ระยะเวลาบอกคุณว่าราคาของพันธบัตรจะเปลี่ยนแปลงมากน้อยเพียงใด ความโค้งบอกคุณว่าระยะเวลานั้นเปลี่ยนแปลงมากน้อยเพียงใดเมื่ออัตราดอกเบี้ยผันผวน

สำหรับนักลงทุน ความโค้งงอเป็น พลังพิเศษในการจัดการความเสี่ยง พันธบัตรที่มีความโค้งงอสูงจะมีมูลค่าเพิ่มขึ้นมากเมื่ออัตราดอกเบี้ยลดลงและจะสูญเสียมูลค่าน้อยลงเมื่ออัตราดอกเบี้ยสูงขึ้นเมื่อเปรียบเทียบกับพันธบัตรที่มีความโค้งงอต่ำ สั้นๆ มันแสดงถึงความโค้งของความสัมพันธ์ระหว่างราคาและผลตอบแทน ทำหน้าที่เป็นเกราะป้องกันที่ปกป้องคุณในช่วงความผันผวนของตลาด

ทำไมระยะเวลาไม่เพียงพอ: ข้อจำกัดของการคิดเชิงเส้น

ผู้เริ่มต้นส่วนใหญ่เริ่มต้นด้วยระยะเวลาเพื่อลดความเสี่ยงจากอัตราดอกเบี้ย หากพันธบัตรมีระยะเวลา 5 ปี การเพิ่มขึ้น 1% ในอัตราควรนำไปสู่การลดลง 5% ในราคาในทางทฤษฎี

อย่างไรก็ตาม การคำนวณนี้เป็นการประมาณเชิงเส้น – มันสมมติว่าความสัมพันธ์เป็นเส้นตรง ในความเป็นจริง ความสัมพันธ์เป็นโค้ง.

- ระยะเวลา คือ เส้นตรง (สัมผัส) ที่จุดเฉพาะบนโค้งหนึ่ง.

- ความโค้ง คำนึงถึงการโค้งงอในเส้นโค้งนั้น。

เมื่ออัตราดอกเบี้ยเคลื่อนตัวออกห่างจากจุดเริ่มต้น การคาดการณ์ระยะเวลาตามเส้นตรงจะมีความไม่ถูกต้องมากขึ้น ความโค้งช่วยแก้ไขความผิดพลาดนี้

การทำงานของความโค้งในภาษาอังกฤษที่เข้าใจง่าย

คิดถึงความโค้งเป็นอัตราการเปลี่ยนแปลงของความไวของพันธบัตรของคุณ

- เมื่ออัตราดอกเบี้ยลดลง: ราคาพันธบัตรจะเพิ่มขึ้น หากพันธบัตรมีความโค้งสูง ราคาจะเพิ่มขึ้นเร็วกว่าที่ระยะเวลาจะบ่งชี้

- เมื่ออัตราดอกเบี้ยสูงขึ้น: ราคาพันธบัตรลดลง หากพันธบัตรมีความโค้งสูง ราคาจะลดลงช้ากว่าที่ระยะเวลาจะแนะนำ.

โดยพื้นฐานแล้ว ความโค้งงอเป็นคุณลักษณะที่เป็นประโยชน์สำหรับผู้ถือพันธบัตรส่วนใหญ่ มันเหมือนกับการมีประกันที่ช่วยเพิ่มผลกำไรและบรรเทาความเสียหายของคุณ

ความโค้งเชิงบวก vs. ความโค้งเชิงลบ: มีความแตกต่างกันอย่างไร?

พันธบัตรไม่ได้มีพฤติกรรมเหมือนกันทั้งหมด การเข้าใจทิศทางของกราฟเป็นสิ่งสำคัญสำหรับการจัดการพอร์ตโฟลิโอ

ความโค้งเชิงบวก

พันธบัตรมาตรฐานส่วนใหญ่ (พันธบัตรที่จ่ายดอกเบี้ยปกติและเงินต้นเมื่อถึงกำหนด) มีความโค้งเชิงบวก

- ประโยชน์: เมื่อผลตอบแทนลดลง ราคาจะเพิ่มขึ้นในอัตราที่เร่งตัว.

- ความปลอดภัย: เมื่อผลผลิตเพิ่มขึ้น ราคา จะลดลงในอัตราที่ช้าลง.

ความโค้งลบ

สิ่งนี้มักเกิดขึ้นใน พันธบัตรที่เรียกเก็บได้ หรือ หลักทรัพย์ที่มีหลักประกันจากจำนอง (MBS)。

- ความเสี่ยง: เมื่ออัตราดอกเบี้ยลดลง ผู้ที่ออกพันธบัตรมีแนวโน้มที่จะเรียก (ชำระคืน) พันธบัตรก่อนกำหนดเพื่อรีไฟแนนซ์ในอัตราที่ต่ำกว่า ซึ่งจะจำกัดการเพิ่มขึ้นของราคา.

- รูปทรง: เส้นอัตราผลตอบแทนราคาจะเรียบหรือแม้แต่ลดลงเมื่ออัตราดอกเบี้ยลดลง.

| ฟีเจอร์ | ความโค้งเชิงบวก | ความโค้งเชิงลบ |

| การเคลื่อนไหวของราคา (อัตราลดลง) | ราคาขึ้นอย่างมีนัยสำคัญ | การขึ้นของราคาอยู่ในขอบเขต/มีเพดาน |

| การเคลื่อนไหวของราคา (อัตราเพิ่มขึ้น) | ราคาลดลงอย่างสง่างาม | ราคาลดลงอย่างรวดเร็ว |

| ตัวอย่างทั่วไป | พันธบัตรรัฐบาลสหรัฐ, พันธบัตรบริษัท | พันธบัตรที่เรียกคืนได้, MBS |

ทำไมผู้ค้าและนักลงทุนควรใส่ใจเกี่ยวกับความโค้ง?

หากคุณเป็นนักลงทุนที่ซื้อและถือพันธบัตรรัฐบาล 2 ปี ความโค้งอาจไม่ทำให้คุณนอนไม่หลับ อย่างไรก็ตาม หากคุณบริหารพอร์ตโฟลิโอหรือซื้อขายอย่างกระตือรือร้น นี่คือเมตริกที่สำคัญสำหรับสามเหตุผล:

การประเมินความเสี่ยงที่ดีกว่า

ในช่วงเวลาที่ตลาดมีความผันผวนสูง ระยะเวลาที่ใช้เพียงอย่างเดียวจะประเมินค่าต่ำเกินไปว่า พอร์ตการลงทุนของคุณอาจสูญเสียมากเพียงใดหากอัตราเพิ่มขึ้นอย่างรวดเร็ว การวัดความโค้งจะให้สถานการณ์ที่เลวร้ายที่สุดซึ่งมีพื้นฐานอยู่ในความเป็นจริง

การจับผลผลิตที่เพิ่มขึ้น

ผู้ค้าโดยทั่วไปมักมองหาพันธบัตรที่มีความโค้งมากขึ้นเมื่อพวกเขาคาดหวังว่าดอกเบี้ยจะผันผวน แม้ว่าทิศทางการเคลื่อนไหวของอัตราจะไม่แน่นอน แต่การได้รับความโค้งสามารถให้ข้อได้เปรียบเล็กน้อยในผลตอบแทนรวม

การป้องกันพอร์ตโฟลิโอ

นักลงทุนสถาบันใช้ความโค้งเพื่อให้สอดคล้องกับสินทรัพย์และหนี้สินของตน โดยการทำให้ระยะเวลาและความโค้งของพอร์ตการลงทุนของตนสอดคล้องกับภาระผูกพันในการชำระเงินในอนาคต พวกเขาสามารถปกป้องตัวเองจากการเปลี่ยนแปลงขนานครั้งใหญ่ในเส้นอัตราผลตอบแทน

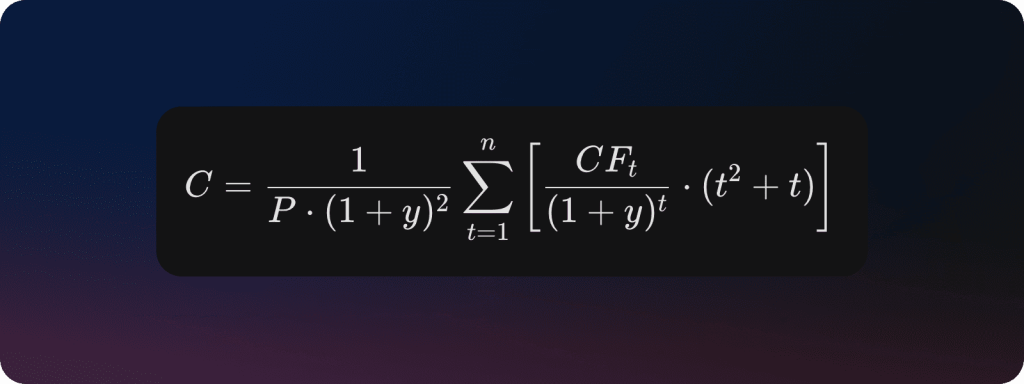

วิธีการคำนวณความโค้ง

ในขณะที่แพลตฟอร์มการซื้อขายส่วนใหญ่ (เช่น Bloomberg หรือ Reuters) คำนวณสิ่งนี้ให้คุณ แต่มันมีประโยชน์ที่จะเข้าใจคณิตศาสตร์ สูตรสำหรับความโค้ง (C) เกี่ยวข้องกับอนุพันธ์อันดับสองของราคาพันธบัตร (P) เทียบกับผลตอบแทน (y):

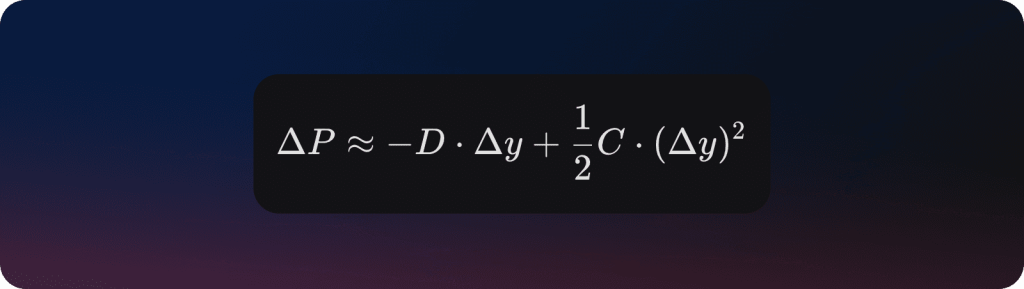

ในการหาการเปลี่ยนแปลงที่แท้จริงในราคาของพันธบัตร คุณต้องรวมระยะเวลา (Duration) และความโค้ง (Convexity):

- ส่วนแรก (-D x Delta(y)) คือผลกระทบจากระยะเวลา.

- ส่วนที่สอง (½ C x Delta(y)^2) คือการปรับความโค้ง. โปรดทราบว่าเนื่องจากการเปลี่ยนแปลงในผลตอบแทน (Delta(y)) ถูกยกกำลังสอง การปรับนี้มักจะเป็นบวกสำหรับพันธบัตรมาตรฐาน ไม่ว่าจะเป็นอัตราเพิ่มขึ้นหรือลดลง.

ข้อผิดพลาดทั่วไปที่ผู้เริ่มต้นทำกับความโค้ง

- การมองข้ามในสภาพแวดล้อมที่อัตราต่ำ: เมื่ออัตราดอกเบี้ยใกล้ศูนย์ การเคลื่อนไหวเล็กน้อยในอัตราจะหมายถึงการเปลี่ยนแปลงเปอร์เซ็นต์ที่ใหญ่โต ในสภาพแวดล้อมเหล่านี้ ความโค้งจะมีอิทธิพลมากขึ้น

- การสมมติว่ามากกว่ามักจะดีกว่า: แม้ว่าความโค้งเชิงบวกจะดีโดยทั่วไป แต่พันธบัตรที่มีความโค้งสูงมักจะเสนอผลตอบแทนที่ต่ำกว่าจนถึงวันครบกำหนด เพราะตลาดเรียกเก็บเงินจากคุณสำหรับการป้องกันเพิ่มเติมนั้น คุณกำลังจ่ายเบี้ยประกันภัยสำหรับความโค้งนั้นอยู่จริงๆ

- สับสนกับความผันผวน: ความโค้งไม่ใช่ความผันผวนเอง; แต่มันเป็นคำอธิบายว่าพันธบัตรตอบสนองต่อความผันผวนอย่างไร.

ผลกระทบของการปรับอัตราดอกเบี้ย 2% ต่อพันธบัตรประเภทต่างๆ

เพื่อช่วยให้คุณเห็นภาพว่าความโค้งแปลเป็นการเคลื่อนไหวของดอลลาร์ในโลกแห่งความเป็นจริงได้อย่างไร นี่คือตารางเปรียบเทียบ

นี่หมายถึงการเปลี่ยนแปลงแบบขนานซึ่งอัตราดอกเบี้ยพุ่งสูงขึ้นทันที 2% (200 จุดฐาน) สังเกตว่าการปรับความโค้งจริงๆ ช่วยให้พันธบัตรที่มีความโค้งสูงหลีกเลี่ยงการขาดทุนที่ลึกกว่ามาก

| ประเภทพันธบัตร | ราคาตลาด | ระยะเวลา (ปี) | ความโค้ง | การสูญเสียจากระยะเวลา | การประหยัดจากความโค้ง | การเปลี่ยนแปลงราคาทั้งหมด |

| พันธบัตรรัฐบาล 2 ปี | $1,000 | 1.9 | 4.5 | -$38.00 | +$0.90 | -$37.10 |

| พันธบัตรรัฐบาล 10 ปี | $1,000 | 8.2 | 85.0 | -$164.00 | +$17.00 | -$147.00 |

| พันธบัตรศูนย์คูปอง 30 ปี | $1,000 | 29.5 | 920.0 | -$590.00 | +$184.00 | -$406.00 |

การเคลื่อนไหวเชิงกลยุทธ์สำหรับนักลงทุน

หากคุณคาดหวังถึงความผันผวนของตลาดที่สูง แต่ไม่แน่ใจว่าดอกเบี้ยจะไปในทิศทางไหน คุณต้องการเพิ่มความโค้งของพอร์ตการลงทุนของคุณ คุณสามารถทำได้โดย:

- การซื้อพันธบัตรแบบศูนย์คูปอง: พันธบัตรเหล่านี้มีความโค้งสูงสุดสำหรับอายุการใช้งานที่กำหนดใดๆ.

- กลยุทธ์ Barbell: แทนที่จะซื้อพันธบัตร 10 ปี ให้ซื้อพันธบัตรผสมระหว่าง 2 ปีและ 30 ปี ส่วนของ 30 ปีจะให้การเพิ่มความโค้งที่มีขนาดใหญ่ซึ่งพันธบัตร 10 ปีมาตรฐานไม่มี

- หลีกเลี่ยงหนี้ที่เรียกคืนได้: หลีกเลี่ยงพันธบัตรที่ผู้ออกสามารถซื้อคืนจากคุณได้ เพราะพันธบัตรเหล่านี้มักมีความโค้งลบซึ่งจำกัดผลตอบแทนของคุณในขณะที่ทำให้คุณเสี่ยงต่อการขาดทุน.

ผลลัพธ์สุดท้าย

ถ้าระยะเวลาเป็นมาตรวัดความเร็วของพอร์ตพันธบัตรของคุณ ความโค้งงอเป็นคะแนนความปลอดภัย ในขณะที่ระยะเวลาให้การประมาณการอย่างรวดเร็วว่าราคาพันธบัตรของคุณจะเคลื่อนที่ไปมากเพียงใดเมื่ออัตราดอกเบี้ยเปลี่ยนแปลง ความโค้งงอจะให้ภาพรวมทั้งหมดโดยคำนึงถึงความโค้งตามธรรมชาติของตลาด

สำหรับนักลงทุนทั่วไป ข้อสรุปนั้นง่ายดาย: ความโค้งเชิงบวกเป็นข้อได้เปรียบเชิงโครงสร้าง มันทำให้แน่ใจว่าเมื่ออัตราลดลง กำไรของคุณจะมากกว่าที่คาดไว้ และเมื่ออัตราเพิ่มขึ้น ขาดทุนของคุณจะน้อยกว่าที่การคำนวณระยะเวลาง่ายๆ จะคาดการณ์ไว้