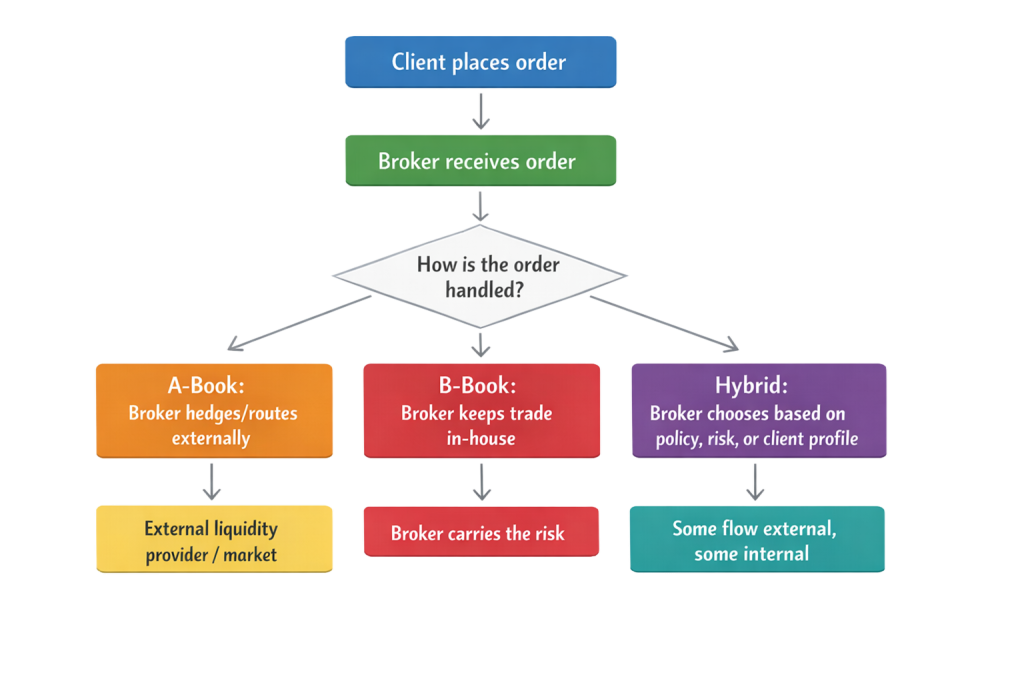

Modelos A-Book, B-Book e Híbrido são diferentes maneiras pelas quais um corretor lida com as negociações dos clientes e gerencia o risco que vem com elas. Em um modelo A-Book, o corretor repassa o risco de mercado para um provedor de liquidez externo. Em um modelo B-Book, o corretor mantém a negociação internamente e assume o lado oposto da posição do cliente. Um modelo Híbrido combina ambas as abordagens, roteando algumas ordens externamente e internalizando outras com base na política de risco do corretor, no perfil do cliente ou nas condições de mercado. Esses rótulos são jargões da indústria usados com mais frequência em corretoras de FX e CFD de varejo, em vez de categorias regulatórias formais.

Essa é a resposta prática. O que torna o tópico importante é tudo o que decorre dele: como um corretor ganha dinheiro, onde podem aparecer conflitos de interesse, como a qualidade da execução é tratada, quanta transparência um trader recebe e quanto risco o corretor está assumindo em seus próprios livros. Em outras palavras, isso não é apenas um detalhe operacional escondido nos bastidores. Isso molda a relação entre corretor e cliente.

Se você está comparando corretores, lançando uma corretora ou simplesmente tentando entender como os pedidos são realmente tratados por trás da interface da plataforma, esses três modelos valem a pena ser compreendidos corretamente. Eles afetam preços, execução, confiança e a estabilidade dos negócios a longo prazo.

A diferença à primeira vista

| Modelo | Como os pedidos são tratados | Quem assume o risco de mercado? | Perfil principal de receita | Principal preocupação |

| A-Book | Pedidos são cobertos ou encaminhados externamente | Fornecedor de liquidez externo / mercado | Comissões, margens de spread, receita baseada em volume | Margens mais baixas, maior dependência da qualidade do fluxo |

| B-Book | Pedidos são mantidos internamente | O corretor | Spreads, PnL internalizado, taxas | Potencial conflito de interesse |

| Híbrido | Alguns pedidos são encaminhados externamente, outros são internalizados | Compartilhado entre o corretor e contrapartes externas | Modelo de receita misto | Requer controles fortes, política de encaminhamento clara e boa supervisão |

A maneira mais simples de imaginar isso

Muitos artigos complicam demais este tópico. A maneira mais fácil de entendê-lo é seguir um pedido de cliente.

Em outras palavras, a verdadeira questão não é se o corretor “executa” sua ordem. Todos os corretores fazem isso de alguma forma. A verdadeira questão é para onde vai o risco após a ordem ser aceita.

Por que esses modelos são importantes

Para os traders, o modelo de execução afeta mais do que a maioria das pessoas percebe. Ele pode influenciar os spreads, o slippage, a qualidade da execução, os incentivos do corretor e como a empresa se comporta quando os mercados se tornam voláteis.

Para os corretores, o modelo de execução é ainda mais fundamental. Ele determina como a empresa gerencia a exposição, como ganha receita, quanta tecnologia precisa e quão cuidadosamente deve monitorar a conduta e a conformidade.

É por isso que a discussão sobre A-Book/B-Book continua surgindo. Não é apenas uma distinção técnica de nicho. É uma das maneiras mais claras de entender como um negócio de corretagem é projetado.

Modelo A-Book: o corretor roteia o risco

Em uma configuração A-Book, o corretor não mantém o risco de mercado do cliente em seus próprios livros. Em vez disso, ele compensará ou protegerá essa exposição com uma parte externa, tipicamente um provedor de liquidez ou outra contraparte institucional. No uso da indústria, essa é a ideia central por trás da execução A-Book.

É por isso que os corretores A-Book são frequentemente descritos como mais “semelhantes a uma agência” ou mais alinhados com o volume dos clientes do que com as perdas dos clientes. Sua principal fonte de renda geralmente vem de comissões, markups de spread ou receita de execução relacionada, em vez de assumir o outro lado de uma negociação vencedora ou perdedora de um cliente.

O que os traders geralmente gostam sobre A-Book

O apelo é óbvio. Se o corretor não estiver armazenando o risco do cliente, o corretor tem menos incentivo econômico direto para se beneficiar de uma perda do cliente naquela negociação específica. Isso tende a fazer com que o A-Book pareça mais limpo e mais transparente.

Também pode ser atraente para traders que se importam muito com o acesso ao mercado, especialmente se utilizarem tamanhos maiores, estratégias mais ativas, ou desejarem preços que reflitam mais de perto as condições de liquidez externa.

A troca

A-Book não é um modelo mágico “perfeito”. Geralmente, tem margens mais baixas do que B-Book e depende mais fortemente do acesso do corretor a uma boa liquidez externa, roteamento eficiente e volume de negociação sustentável. Isso também pode significar mais exposição a condições reais de mercado, incluindo spreads mais amplos ou slippage durante mercados voláteis.

E mesmo em um ambiente A-Book, o corretor ainda tem sérias responsabilidades de manuseio de ordens. Nos EUA, a SEC afirma que os corretores são legalmente obrigados a buscar a melhor execução razoavelmente disponível para as ordens dos clientes. Na Europa e no Reino Unido, as regras de melhor execução e conflitos continuam a se aplicar quando as empresas manuseiam ordens de clientes.

Assim, o A-Book reduz um tipo de conflito, mas não elimina a necessidade de supervisão, revisão de execução ou divulgações claras.

Modelo B-Book: o corretor mantém a negociação internamente

Em um modelo B-Book, o corretor internaliza a negociação em vez de enviar o risco externamente. Em linguagem simples, isso significa que o corretor é a contraparte da posição do cliente e mantém essa exposição em seus próprios livros em vez de se proteger imediatamente. Esse é o significado básico da execução B-Book na indústria.

Este é o modelo que tende a gerar as reações mais fortes, principalmente porque o conflito é mais fácil de ver. Se o corretor mantiver o risco, então as perdas do cliente podem se tornar parte da economia do corretor.

Dito isso, é aqui que muitos artigos se tornam preguiçosos. Eles tratam o B-Book como automaticamente antiético, o que não é preciso.

B-Book não é automaticamente abusivo

Um corretor B-Book não é inerentemente desonesto. A internalização em si não é a mesma coisa que manipulação. Muitas empresas internalizam o fluxo e ainda operam dentro de fortes estruturas regulatórias e de supervisão. O que importa é como o modelo é gerido: integridade de preços, qualidade de execução, divulgações, controles internos, gerenciamento de reclamações e se a empresa gerencia conflitos de maneira responsável.

Os reguladores há muito tratam conflitos de interesse como uma questão central de supervisão. A SEC destacou como as corretoras que tanto facilitam as negociações dos clientes quanto se envolvem em atividades proprietárias podem criar conflitos, incluindo a internalização a preços desfavoráveis para os clientes ou outras condutas que colocam os interesses da empresa à frente dos clientes. A FINRA também continua a enquadrar a gestão de conflitos como uma obrigação de supervisão contínua para empresas e corretores.

Por que os corretores usam B-Book

A resposta é simples: pode ser comercialmente eficiente.

Se um corretor tem fluxo suficiente e correspondência interna suficiente, pode compensar parte do risco do cliente contra outras posições de clientes e gerenciar o restante dentro de limites definidos. Isso pode tornar os spreads mais competitivos, reduzir os custos de hedge externo e melhorar as margens. Fontes de educação da indústria também observam que os corretores geralmente reservam o hedge externo para fluxos que consideram mais difíceis ou mais perigosos de armazenar internamente.

O verdadeiro risco do B-Book

O problema não é o modelo em si. O problema é a tentação de executá-lo mal.

Se uma empresa está subcapitalizada, carece de controles adequados ou trata as perdas dos clientes como o plano de negócios em vez de um componente de risco entre muitos, a confiança se quebra rapidamente. É por isso que discussões sobre B-Book quase sempre levam a perguntas sobre ética, regulamentação e transparência.

Modelo híbrido: o que muitos corretores realmente fazem

Um corretor Híbrido usa ambas as abordagens. Alguns pedidos são direcionados externamente, e alguns são internalizados. A decisão de roteamento pode depender do tamanho da negociação, do comportamento do cliente, do tipo de estratégia, da lucratividade histórica, do risco de concentração ou dos limites de risco interno. Na educação de FX para varejo, isso é muitas vezes descrito como a configuração mais comum do mundo real, pois oferece aos corretores mais flexibilidade do que qualquer um dos modelos puros por si só.

A flexibilidade é o ponto principal.

Um corretor pode decidir que determinado fluxo é melhor protegido externamente porque é grande, consistentemente lucrativo, sensível à latência ou difícil de armazenar com segurança. Outro fluxo pode ser internalizado porque é pequeno, equilibrado em relação a outras posições ou economicamente eficiente mantê-lo internamente.

Por que o híbrido se tornou tão comum

Porque reflete a realidade melhor do que o debate “A-Book puro vs. B-Book puro”.

A maioria das corretoras não quer se comprometer com uma filosofia de roteamento rígida para todos os clientes e todas as condições. Elas querem flexibilidade. Um modelo híbrido permite que elas mantenham essa flexibilidade enquanto ajustam a exposição dinamicamente.

Isso é útil comercialmente, mas também cria um ônus de governança mais pesado. Uma vez que um corretor está tomando decisões de roteamento entre segmentos de clientes, ele precisa de políticas internas fortes, bom monitoramento, lógica defensável e trilhas de auditoria limpas. Caso contrário, o modelo começa a parecer arbitrário ou, pior, oportunista.

Qual modelo é melhor?

Não há um vencedor universal.

A-Book geralmente soa melhor para os traders porque parece mais limpo e menos conflituoso. B-Book pode ser perfeitamente legítimo, mas requer um grau mais alto de confiança nos controles e na conduta do corretor. O modelo híbrido é frequentemente o mais prático, mas também é o mais difícil de julgar de fora, porque um cliente raramente vê a lógica completa de roteamento.

Uma pergunta melhor não é “Qual modelo é o melhor?” mas sim:

Qual modelo está sendo executado de forma transparente, competente e sob supervisão real?

Essa geralmente é a lente mais útil.

Mitos comuns que confundem a discussão

Mito 1: Um A-Book significa que o corretor não tem conflitos

Não exatamente. A A-Book remove o incentivo direto para lucrar com a perda de um cliente específico, mas o corretor ainda enfrenta conflitos em torno do roteamento, qualidade de execução, incentivos e manuseio de ordens. Os reguladores continuam a tratar a melhor execução e a gestão de conflitos como obrigações contínuas, não como caixas que as empresas marcam uma vez e esquecem.

Mito 2: B-Book significa que o corretor é uma fraude

Também não é verdade. Um corretor pode internalizar fluxo e ainda operar de maneira justa. A verdadeira questão é se a empresa executa esse modelo com preços adequados, divulgações, supervisão e proteções ao cliente. A internalização se torna um problema quando é combinada com comportamentos abusivos, controles deficientes ou condutas enganosas.

Mito 3: Híbrido significa apenas “B-Book secreto”

Isso é simplista demais. Um corretor híbrido pode internalizar algumas ordens e cobrir outras por razões legítimas de gerenciamento de risco. O problema não é que o modelo seja misto. O problema é quando o corretor não está claro sobre como as ordens são tratadas, ou quando as práticas de execução se tornam impossíveis de contestar ou verificar.

Sobre o que a regulamentação realmente se preocupa

Os reguladores geralmente não estruturam a supervisão em torno dos rótulos de marketing “A-Book” e “B-Book.” Eles se concentram nos resultados e controles em torno da execução, conflitos, registros, divulgações e proteção ao cliente.

Essa é a maneira mais séria de olhar para o assunto.

Melhor execução

A SEC diz que os corretores devem buscar a melhor execução razoavelmente disponível para os pedidos dos clientes. A orientação de melhor execução da FINRA também deixa claro que as empresas não podem terceirizar esse dever apenas porque encaminham pedidos para outro lugar. No Reino Unido, a FCA disse explicitamente que, quando um corretor está envolvido no manuseio de pedidos de clientes, conflitos, incentivos e regras de melhor execução estão envolvidos.

Conflitos de interesse

É aqui que os modelos B-Book e Hybrid recebem a maior parte de sua análise. A ESMA anunciou em dezembro de 2025 que lançaria uma Ação de Supervisão Comum com os reguladores nacionais sobre os requisitos de conflitos de interesse da MiFID II na distribuição de instrumentos financeiros. Isso mostra onde está indo a atenção da supervisão: as empresas devem ser capazes de identificar, prevenir e gerenciar conflitos, especialmente em negócios voltados para o varejo.

Dinheiro do cliente e disciplina operacional

No Austrália, a estrutura de relatórios de dinheiro de clientes da ASIC exige que as empresas que mantêm certos fundos de clientes mantenham registros, realizem reconciliações diárias e mensais e relatem certas deficiências. Essas regras não tratam diretamente dos rótulos A-Book ou B-Book, mas mostram quão seriamente os reguladores tratam a disciplina operacional em negócios de negociação alavancada.

Manutenção de registros e auditabilidade

Isso está se tornando um problema maior, não menor. As emendas de registro eletrônico da SEC permitem uma alternativa de trilha de auditoria ao antigo modelo apenas WORM e exigem que os registros eletrônicos sejam produzíveis em um formato razoavelmente utilizável. Em linguagem simples: os reguladores querem que as empresas possam explicar o que aconteceu, quando aconteceu e por quê.

Para onde a indústria está indo

O artigo original tentou transformar isso em uma história de “tendências para 2025”. Uma maneira melhor de enquadrar isso é a seguinte: a direção da viagem é em direção a mais roteamento automatizado, mais auditabilidade e mais escrutínio de conflitos e qualidade de execução.

Isso não é exagero. É uma inferência razoável do que os reguladores estão focando: melhor execução, gerenciamento de conflitos, controles de dinheiro do cliente e manutenção de registros que possam suportar exames. A ESMA tem atualizado a estrutura MiFID II/MiFIR e esclarecido partes do regime de relatórios de melhor execução, enquanto a SEC e a ASIC continuam a enfatizar a manutenção de registros e controles operacionais.

Para os corretores, isso significa que os velhos tempos de explicações de execução imprecisas estão se tornando mais difíceis de defender. Para os traders, isso significa que as perguntas certas estão se tornando mais práticas e mais importantes.

O que os traders devem realmente procurar

A maioria dos traders nunca conseguirá que um corretor forneça um mapa de roteamento completo. Mas isso não significa que você é impotente. Você ainda pode aprender muito sobre como a empresa se explica.

Algumas perguntas importam mais do que as outras:

- O corretor explica claramente se pode internalizar negociações, fazer hedge externamente ou usar uma combinação de ambos?

- Divulga como funciona a precificação, incluindo spreads, markups e quaisquer outros custos relacionados à execução?

- Explique o que pode acontecer em mercados voláteis, incluindo deslizamento, re-cotações ou preenchimentos atrasados?

- A empresa é regulamentada em uma jurisdição que supervisiona ativamente a conduta de negociação no varejo?

- As suas divulgações parecem verdadeiras divulgações de risco, ou como textos de marketing disfarçados de conformidade?

Você não precisa de um modelo teórico perfeito. Você precisa de um corretor cujo modelo de negócios seja compreensível, cuja conduta seja defensável e cujos incentivos não estejam escondidos atrás de uma linguagem vaga.

Considerações finais

Modelos A-Book, B-Book e Híbrido são melhor compreendidos como estruturas de execução e gestão de risco, não apenas palavras da moda dos corretores. A-Book empurra o risco para fora. B-Book mantém o risco internamente. Híbrido faz ambos. Essa é a distinção fundamental.

O que importa depois disso não é apenas o rótulo, mas a qualidade da execução, os controles do corretor, a transparência da configuração e a força do quadro regulatório em torno disso. Um corretor híbrido bem administrado pode ser mais seguro do que um corretor “A-Book-only” mal administrado em condições de supervisão fracas. Uma empresa B-Book regulamentada com divulgações claras e execução justa pode ser mais confiável do que um corretor que se promove como livre de conflitos, mas não consegue explicar suas práticas de roteamento.

Então, a verdadeira lição é simples: não julgue um corretor apenas pelo modelo que afirma usar. Julgue-o pela clareza com que explica esse modelo, como gerencia os riscos por trás dele e se a empresa lhe dá razões para confiar em sua execução.